Lending, Race, and High Income Households

UPDATE 2024-05-22: Added the Misc section to near the end of the post.

The Fair Housing Center of West Michign has published the "The Role of Mortgage Lenders In Shaping Our Neighborhoods" report. The document covers the deep and deepening economic chasm between white and non-white households, at least in terms of home ownership, in Kent County. And the report breaks down the city distinct from the county, and then down to the neighborhood level, which makes it ideal to look at here. It is a well written report, more readable and to-the-point than many housing policy documents.

The TLDR

The conclusion of the report begins with the words:

While the data may be bleak, ...

which, indeed, very much sums it up.

Of course, as a public document, it is obligated to end on some note of hopefulness. Yet the attempt at if-we-can-all-come-together rings very hollow; we have known, essentially, all of this for at least a decade. And for that decade we've accomplished nothing. We had almost a decade of ideal economic circumstances to fundamentally change the housing market during which we did very nearly nothing. Our leaders talked about "hard conversations"; what they did not do was make courageous decisions. Instead of leadership we had reports, such as the "Great Housing Strategies" (2015), and whatever "Housing NOW" was [and ultimately was not]. 😢

The report is a truly depressing and infuriating read.

The Data

The report uses lending data from 2018 - 2021. Since then the lending market has changed, mostly for the worse. It would be incorrect to assume the same patterns will continue apace, yet damage has been done which seems impossible to resolve.

Context: The average 30-year interest rate for a mortgage in 2018 was 4.54%, 2019 3.94%, 2020 3.10%, and in 2021 2.96%. Mortgage rates moved signifiantly in 2022, to 5.34%, and then climbing further in 2023 to 6.81%. In May of 2024 the median rate was 7.21%. The world is always changing, and "the speed of government", desperately needs to learn how to match it.

Likely new, and equally deleterious, trends will emerge.

Gentrification

Yes, this word. 😫 I know. The report uses the term "gentrification" a lot. Blessedly, this report is one of the rare instances where the author(s) provide a definition for this much misappropriated and overused term.

Gentrification: a process in which a poor area (as of a city) experiences an influx of middle-class or wealthy people who renovate and rebuild homes and businesses and which often results in an increase in property values and the displacement of earlier, usually poorer residents.

It is impossible - certainly on this site! 🙂 - not to quibble with this term; particularly the "renovate and rebuild homes and businesses and which often results in an increase in property values". Many people, myself inclueed, are convinced that when you see the renovation and rebuilding of a place it is a response to the increase in value having already happened. By the time you see the contractor vans and construction signs the process is already well underway. This is an important quibble which the report also admits to on page 13:

Gentrifying neighborhoods offer many of the amenities sought by higher income households; they are closer to downtowns, are relatively cheap in comparison to other neighborhoods (and have more room to increase in value), they are in closer proximity to jobs, restaurants, and entertainment

A conveniently overlooked aspect of Gentrification narratives is the scarcity of amenity rich neighborhoods. We should be creating more amenity rich neighborhoods and more housing options in those neighborhoods. In a fierce competition for a scarce resource the competitors with the least advantage are more often than not going to lose. Leveling the advantage is certainly a key strategy - and the focus of this report - however the reduction of scarcity is also a strategy; and one whose tools lie nearer at hand to municipal governments. The expansion of urban amenities to more neighborhoods as well as the densification of amenity rich neighborhoods is something which can be addressed directly by local public policy and investment. The scarcity of these neighborhoods is itself a consequence of local public policy and disinvestment. "Gentrification" is far too often the hand-wringing cry of those holding those status-quo policies in place, exactly the people with the power to change those policies.

The issue of displacement, the problem within "Gentrification" - especially with a more aware economic understanding of its process - is one that needs to be addressed far upstream from when the physical renovation of place occurs.

Some Facts

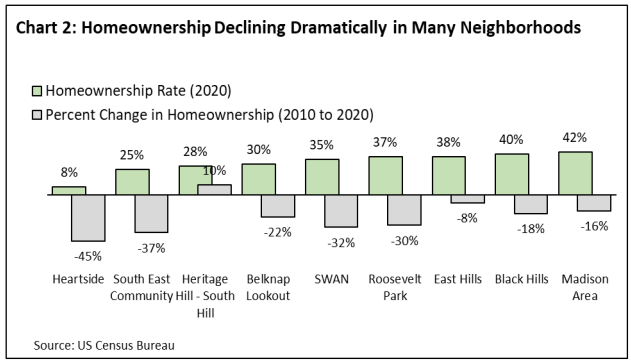

The home ownership rate in Grand Rapids is 56.4%. Within the city home ownership rates vary significantly by neighborhoods; from 8% to 77%. In general the home ownership rate has declined most rapidly in neighborhoods with the lowest rates of home ownership; with the one notable exception of Heritage Hill where home ownership has increased.

Aside: It is only my term, but I like to describe Heritage Hill as in the phase of "late-stage gentrification". Heritage Hill has turned completely over from the discombobulated assembly of multi-unit rentals which it was in my youth to a neighborhood converting back into mansions. The irony of these facts up against to the hue-and-cry of Heritage Hill residents to any kind of land-use reform is saltier than a steaming cup of Bovril.

The Gist

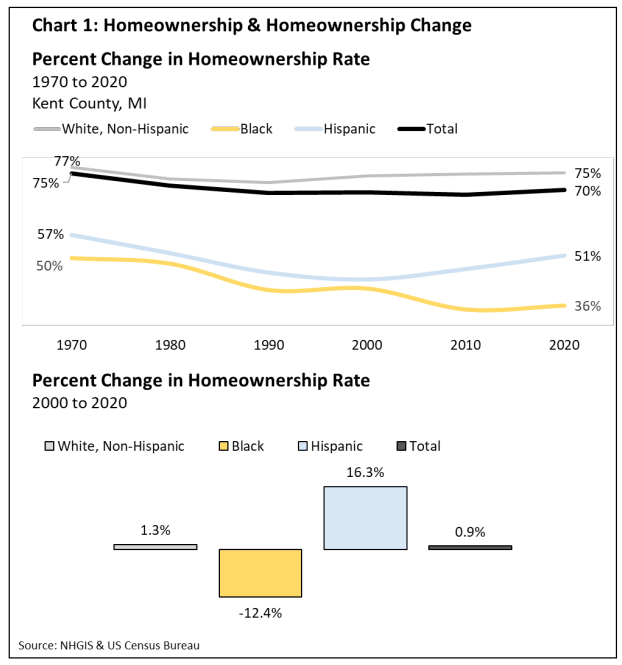

Since 1970 the home ownership gap between black and white (non-hispanic) households has doubled.

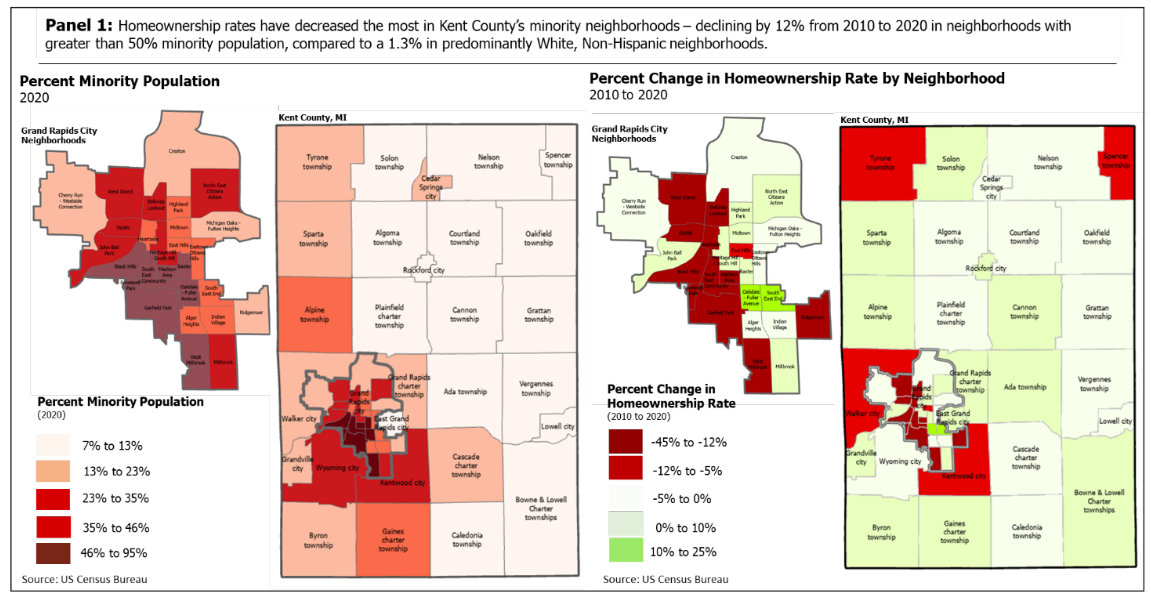

The rate of home ownership in Kent County has declined 1.3%, while in minority neighborhoods it has fallen by 12%.

Aside: I would expect urban home ownership rates to decline faster than the suburbs as higher-density multi-family housing supplants single unit detached housing [which is a good thing, no apologies] but this spread is stunning; especially considering how vanishingly little higher density housing has been constructed. If there were block upon block of higher density housing, then maybe, but there isn't.

- From 2007 to 2021 white borrowers have secured 20x - 30x the number of mortgages as black borrowers, and 10x - 25x the number of hispanic borrowers. Black and hispanic citzens are ~1 in 5 citizens. Again, the spread is scandalous.

- The highest activity is seen in low-to-moderate income neighborhoods, where in the year 2021, mortgage activity increased 7.1% while remaining steady in high income neighborhoods. Additionally more than half of mortgages were to high income households.

What is a "high income household"? A household earning 120% or more of Area Median Income (AMI). AMI is calculated by county, and the AMI for Kent County in 2021 was ~$69,786; so a household earning more than 120% is earning $83,743/yr. Also notable is that Kent county's AMI has been rising streadily, from 2020 to 2021 the AMI rose by 6.18%

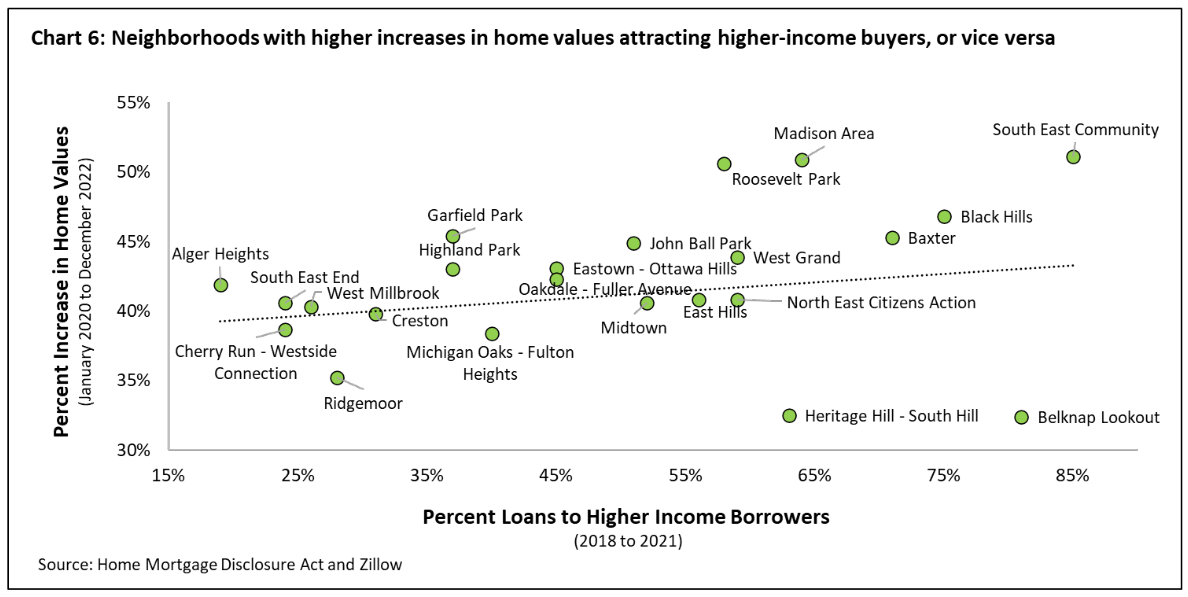

- The most rapid increase in property values and the highest percentage of high income purchasers are skewed toward majority minority neighborhoods.

The Process

The report correlates the overall decline in home ownership, in part, to a variety of factors:

- A decline in two-income households.

- A decreased "in the number of families" ... and odd way to phrase what is a decrease in household size. There are a couple of places in this report the old American Dream idoleology leaks through.

- "shifting generational housing patterns"

... it could be that all three of these points are, ultimately, one point: a decrease in household size.

The focus of this report is, largely setting this data point aside, the impact of mortgage lending, "gentrification", affordability, and "outside investors".

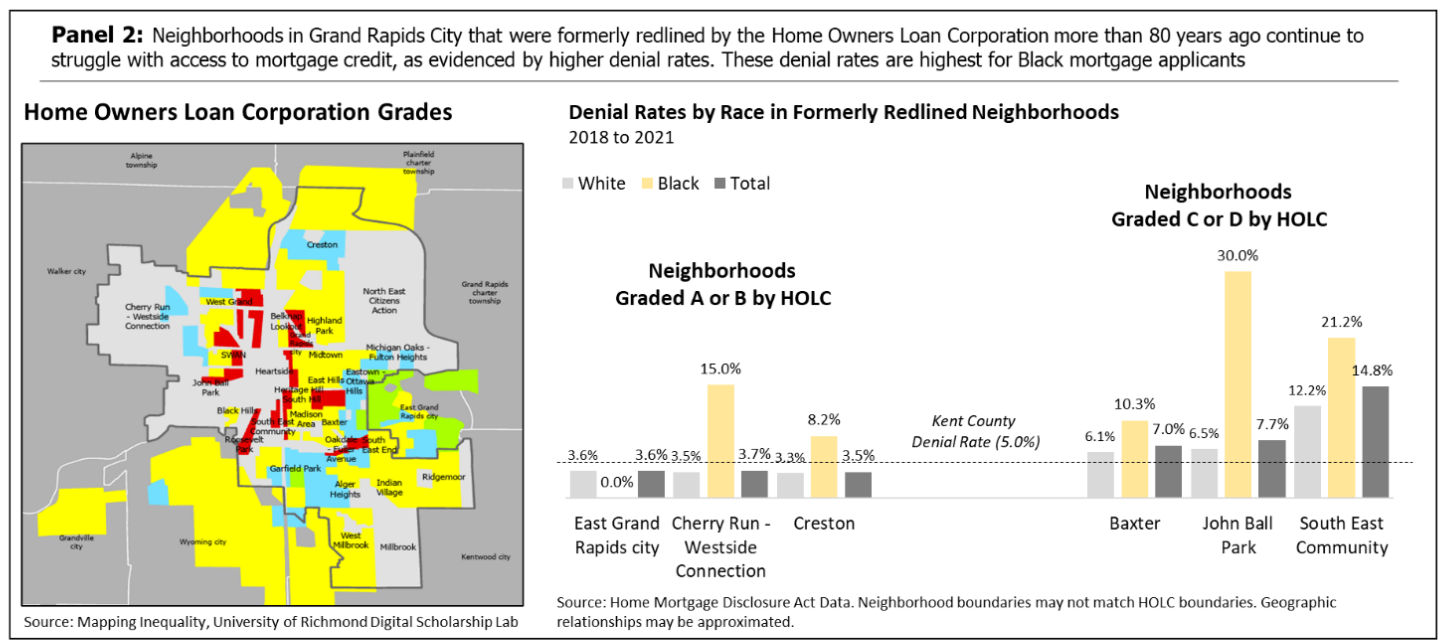

- The denial rate of mortgages originating in historically redlined neighborhoods is higher than in other areas. The overall mortgage denial rate in Kent county is 5.0%, and 5.4% in Grand Rapids; ok. And then you come the denial rate of specific neighborhoods with is ~3X the overall rate; Heartside has an overall denial rate of 15%.

Some of this can be explained by competition for the scarce resource of neighborhoods which has resulted from the misguided public policy of the previous decades. There is this image, from the Housing Next Needs Analysis report, which I have now used in at least a half-dozen posts and articles, here and elsewhere.

The current regime's singular focus on Affordable Housing has been most damaging to the people this regime claims to be the most concerned about. As America's culture and economy has shifted the affluent are returning to the city, a reality our civic leaders have been unwilling to grapple with.

However, before one gets too libertarian, while that scarcity explains some of these trends, there is more. Looking only at higher income households:

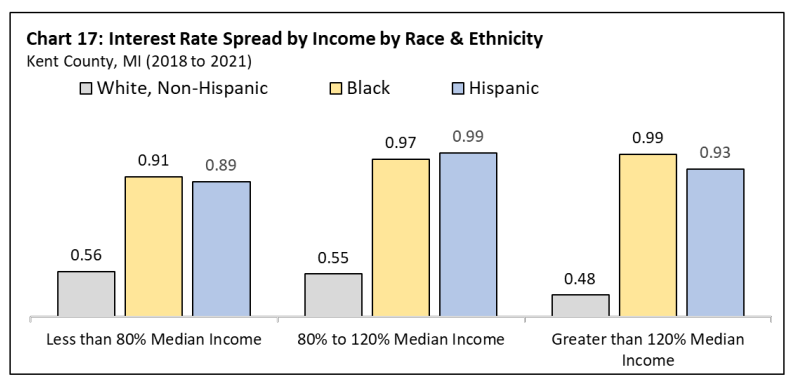

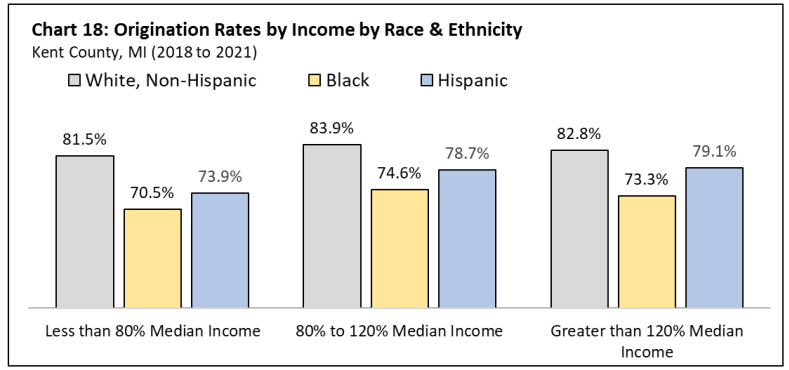

- Higher income citizens of color pay higher interest rates than high income white citizens.

- Higher income citizens of color are less likely to successfully acquire a mortgage.

If that's not enough . . .

Bank branch closures are have been wildly unequal. From 2000 - 2022 suburban communities in Kent county lost 6% of their bank branches, the city of Grand Rapids lost 36% of bank branches, and majority minority neighborhoods lost 78% of their bank branches. The economic revitalization of the city was already underway by 2000. These numbers are staggering.

The overlay of the Home Owners Loan Corporation (HOLC) "redlining" maps onto the denial rate for mortgages speaks for itself.

There is clearly still a problem as pertains to lending practices and race.

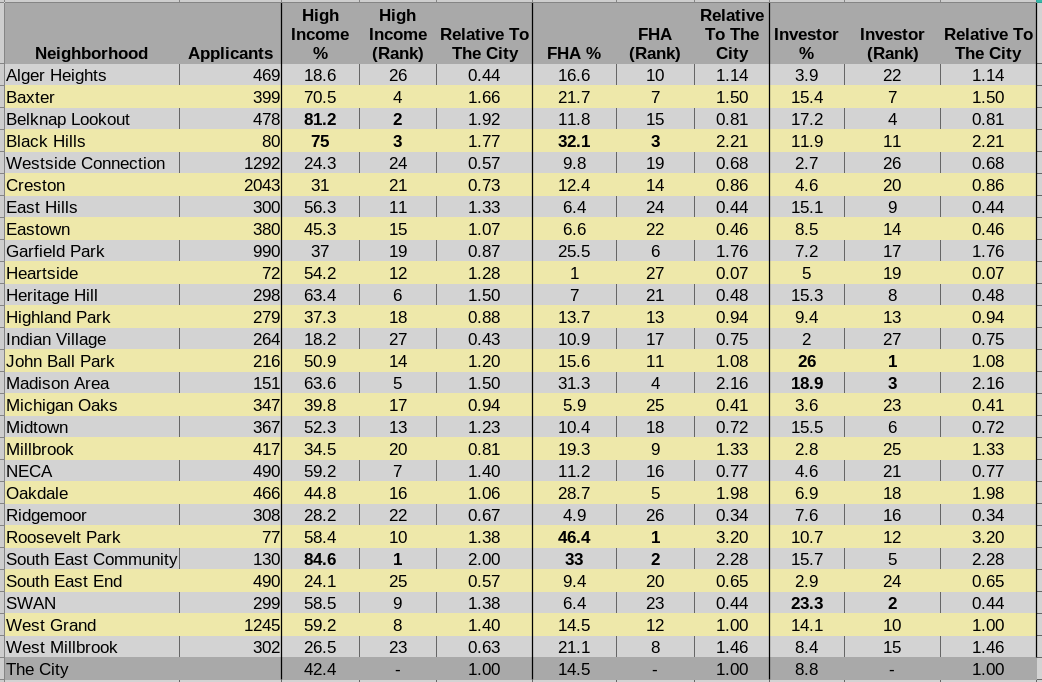

More Data

There is within the report some breakdowns of mortgage originations by high income households, investors, and FHA. I've summarized some of those into a single chart here. The top three neighborhoods for each category are bolded, and they are correlated to the city overall. It is interesting.

Dowload this chart as PDF or ODS

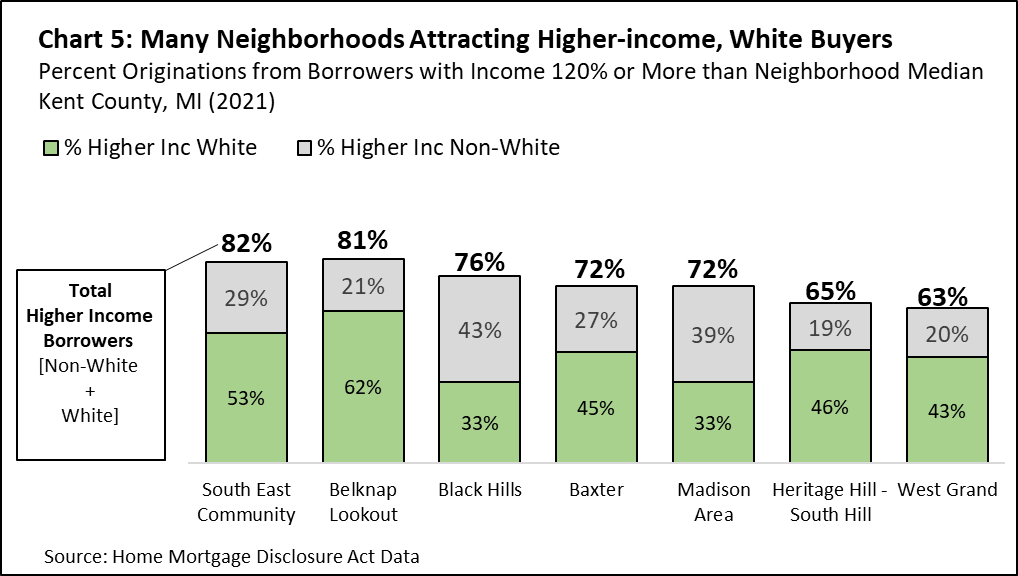

Misc

Someone else spotted this in Chart#5; Black Hills and Madison have majority minority high income purchasers. Often the automatic assumption is that high income borrowers are white, but not always.

Related

- Where high-income and investor buyers are scooping up homes in Grand Rapids, Crains 2024-05-13 - this is an article on the same report

- Why Michigan Should Embrace Zoning Reform, UrbanGR 2023-11-11

- The 2020 Housing Needs Assessment, UrbanGR

- The 2023 Housing Needs Update, UrbanGR

- New Studies Provide Further Evidence That Zoning Reforms Work, Forbes 2023-08-28

- A city's 'walkability' drives real estate values, CNBC 2014

- In the U.S., Walkability Is a Premium Good, CityLab 2016

- Leinberger: Walkable Urbanism Is the Future, ..., Streets BLOG 2012

Notice some of those years? We've known about the scarcity and the desirability of walkable amenity rich neighborhoods for a decade. Why did the Grand Rapids City Commission do so little? Frustrating. The city needs to find a way to build institutional capacity, the ability to move beyond discussion and reporting.